WE MAKE HOME INSURANCE SHOPPING EASY

JERRY BRINGS HOME

THE SAVINGS

WE FIND THE RIGHT COVERAGE FOR YOU

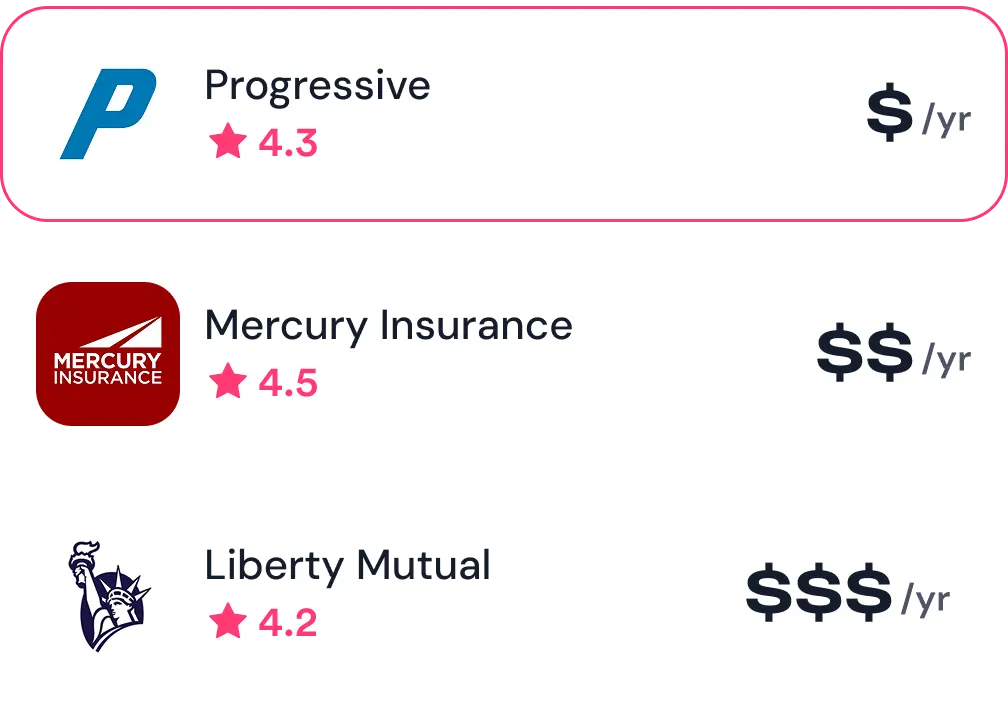

WE MIX AND MATCH

INSURERS TO SAVE A BUNDLE

YOUR DISCOUNTS ARE AUTOMATICALLY STACKED

SHOP SMARTER WITH EXPERT RESOURCES

OVER 5 MILLION CUSTOMERS TRUST JERRY

"Great for shopping home and auto insurance. Pulled rates from multiple insurers and let me tailor my coverage."

"Love the Jerry app. It helped me find a great policy and bundle everything in one easy place."

"Used Jerry for over a year now. Best way to compare and shop for quality home and car insurance, not just the cheapest. Super user-friendly."

"Loved that I could shop home and auto insurance so easily. Happy to have found this gem of an app."

COMMON QUESTIONS

-

How does Jerry compare home insurance quotes?

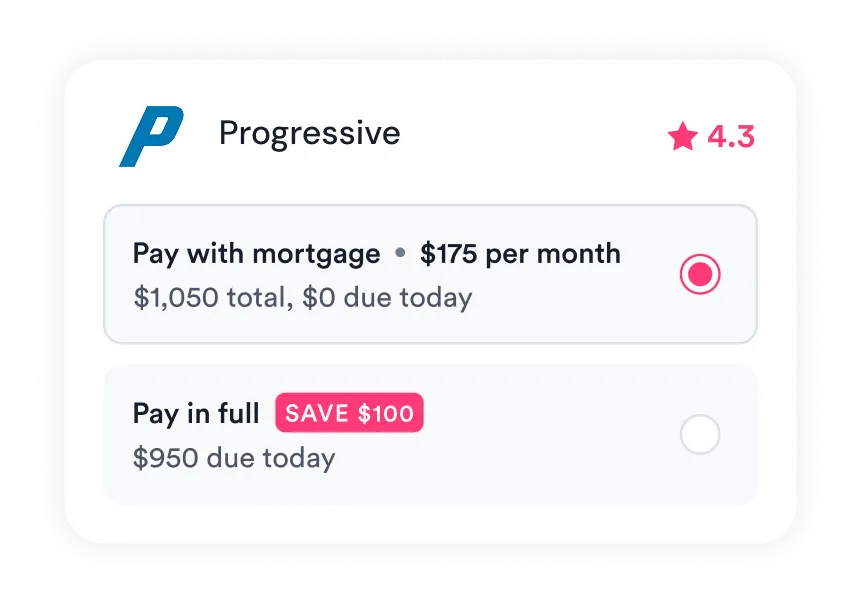

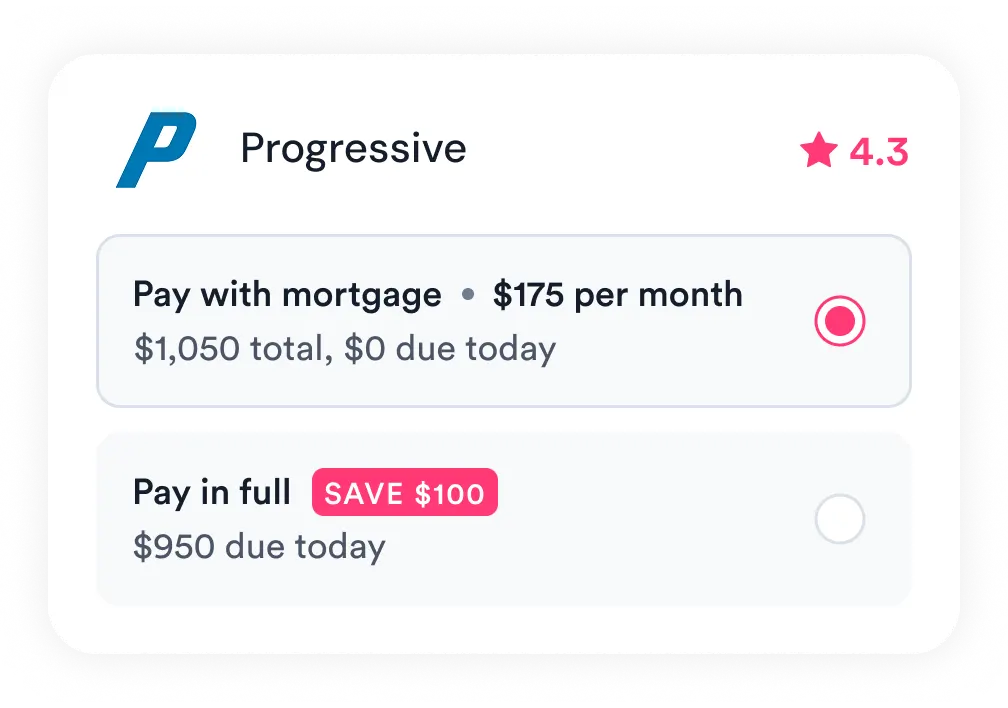

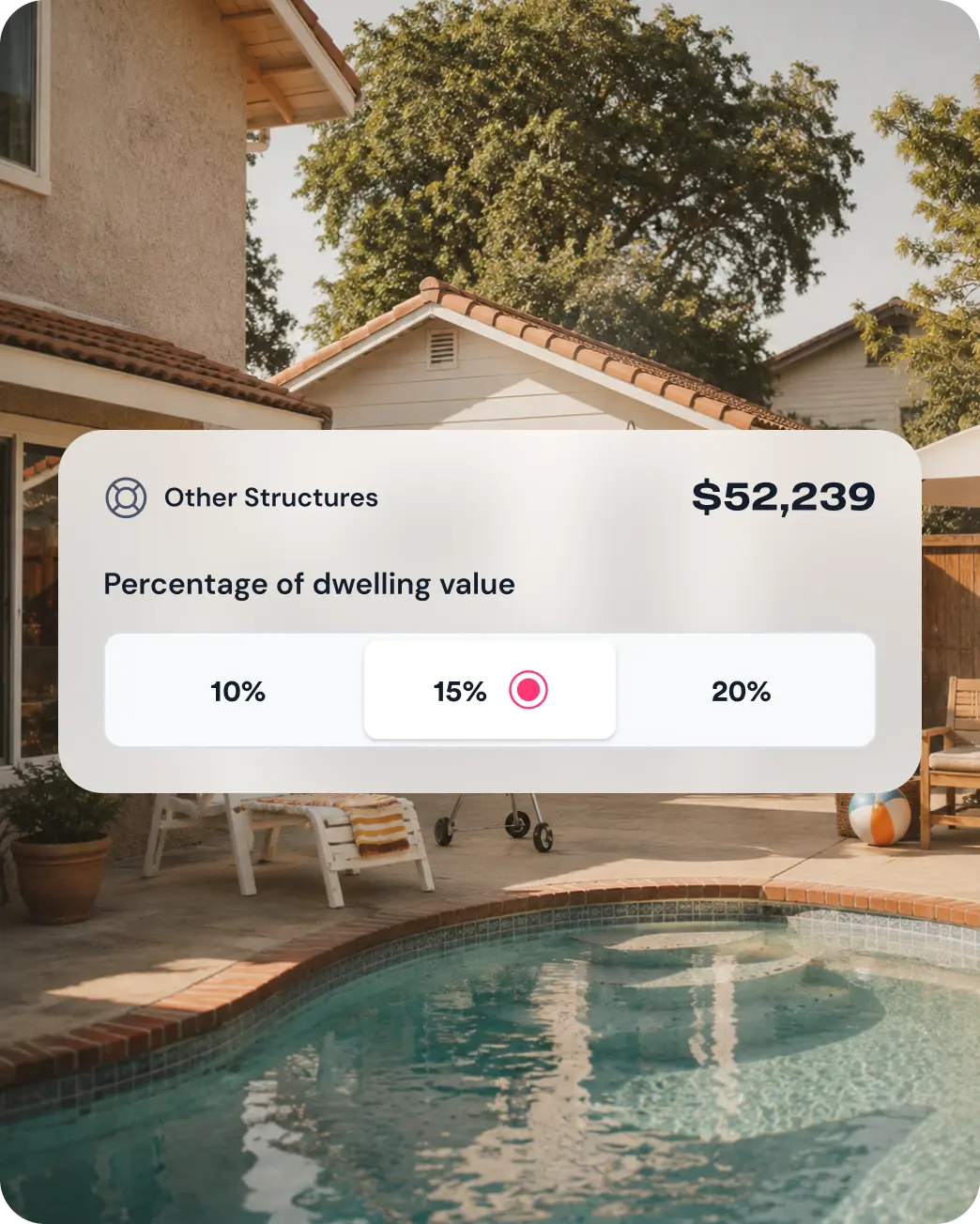

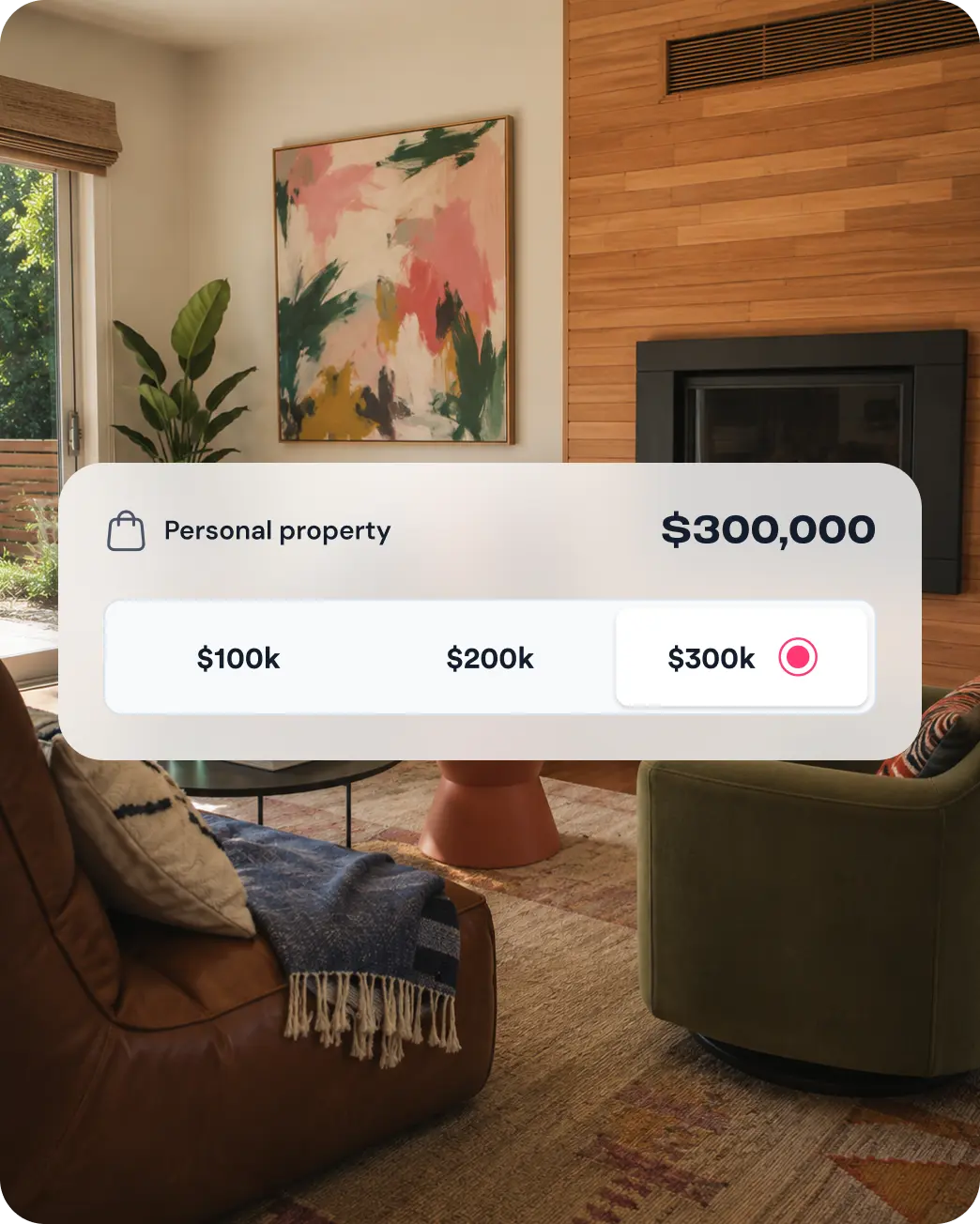

Answer a few questions about your home, and Jerry pulls and shows real-time quotes from dozens of home insurers, with side-by-side prices and coverage options you can adjust on the fly. Raise your deductible or bump up your liability limits and you’ll see the price update. Find a policy you like, and you can buy and switch right in the app. We’ll even cancel your old policy for you.

-

Is Jerry actually free to use?

Yes. Comparing quotes and switching policies through the Jerry app is free. Jerry is a licensed insurance broker, which means insurers pay us a commission when you buy a policy, and that commission has no effect on your price. We also never sell your data, which is why your phone won’t start ringing the moment you finish a quote.

-

How much does home insurance cost per year?

Jerry customers typically pay between $950 and $1,800 per year. Your rate depends on where you live, what it would cost to rebuild your home, the home’s age and roof condition, your claims history, your credit-based insurance score, and the coverage you pick. The best way to find your actual cost is to get a real quote.

-

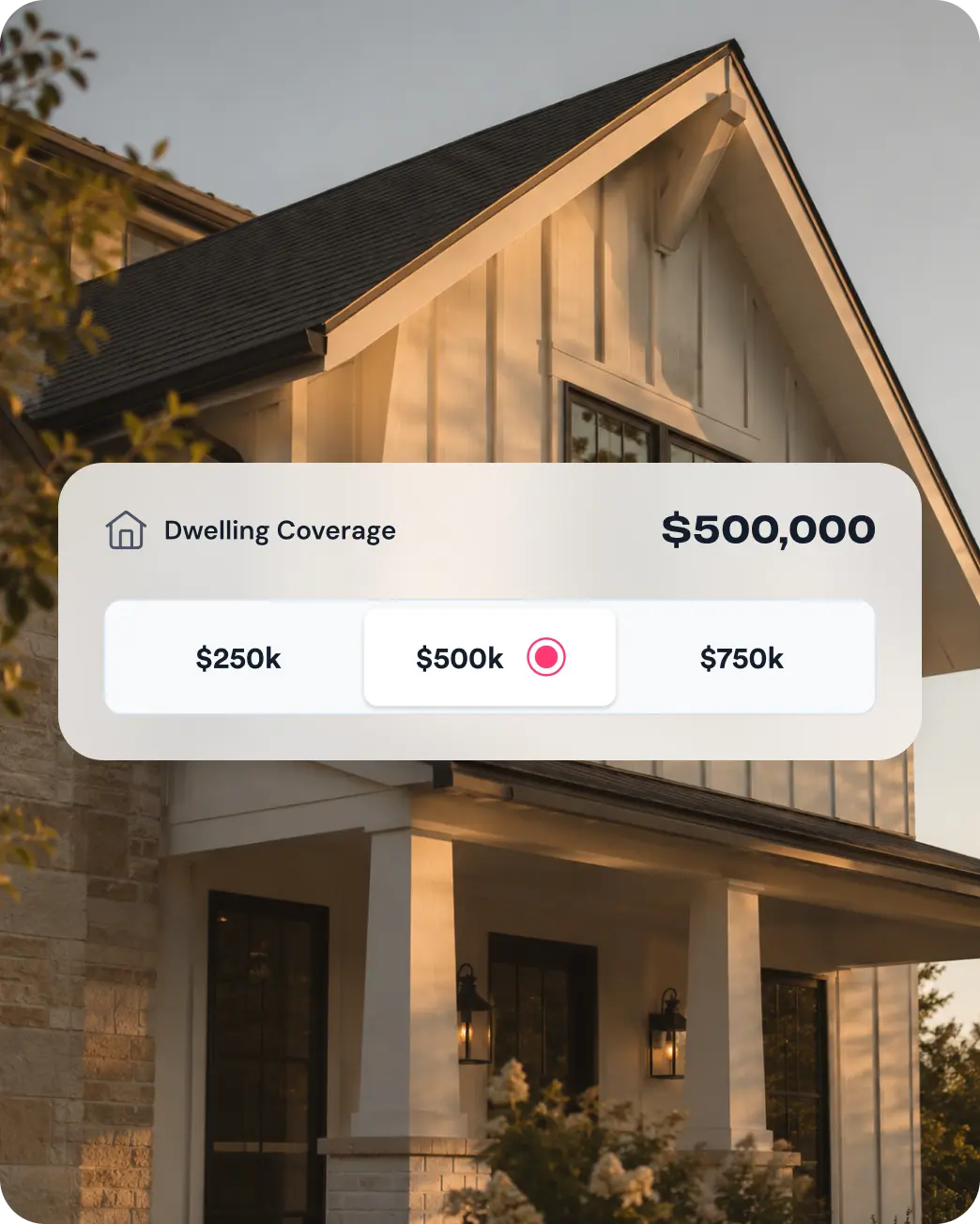

How much dwelling coverage do I need?

Enough to completely rebuild your home at today’s prices —not what your home would sell for. Most insurers want you covered for at least 80% of this amount. Falling short can leave you paying out of pocket after a major loss. Jerry estimates your home’s replacement cost automatically when you quote, so you don’t have to guess (or call a contractor to ask).

-

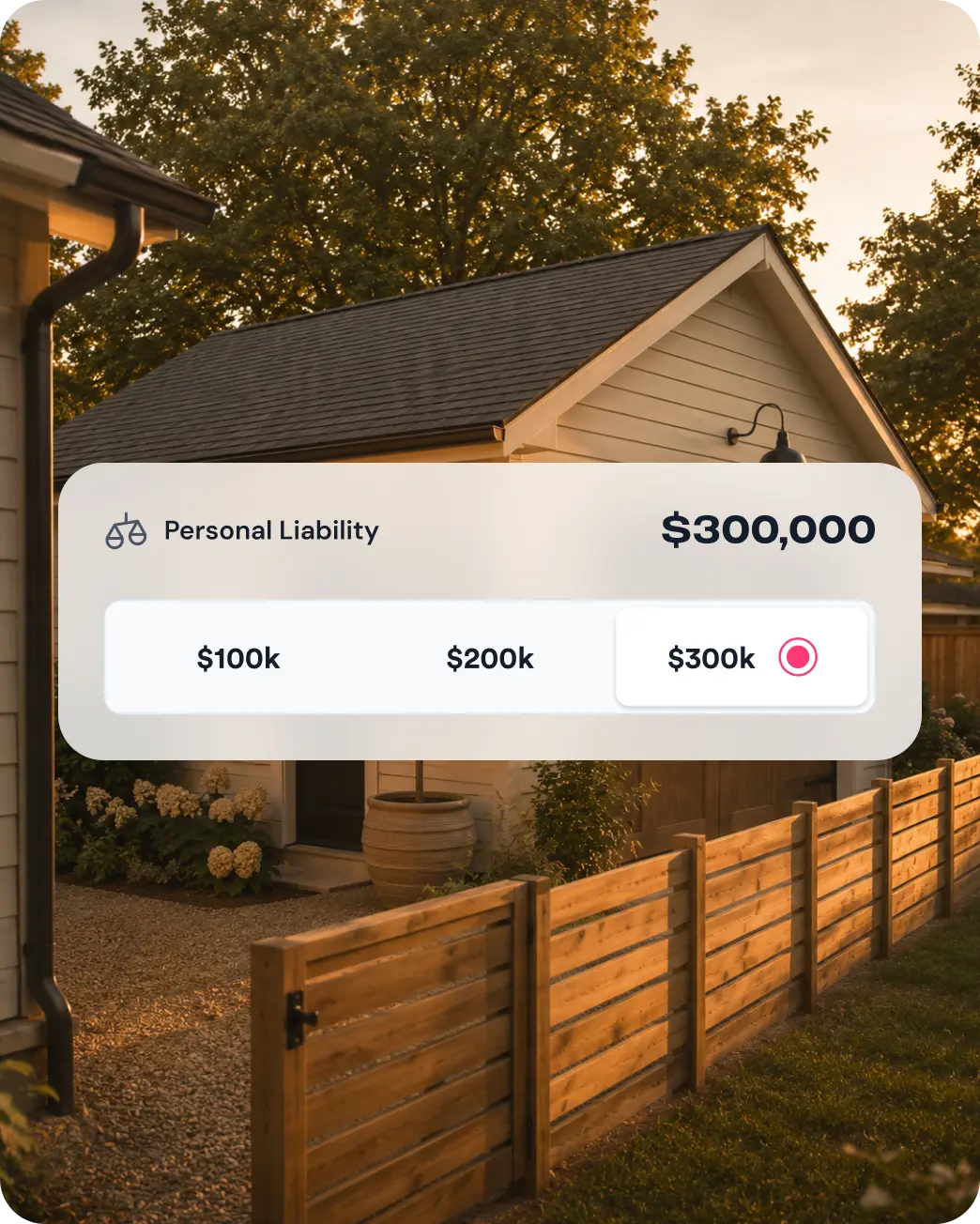

How much liability coverage do I need?

$300,000 is a common starting point. If you have meaningful assets, like a home with equity, savings or retirement accounts, consider $500,000 or higher to protect them from a lawsuit. Umbrella coverage adds another $1M+ for just a few hundred dollars more a year, which is a notably small price so you can sleep through the night.

-

Do I legally need home insurance?

No state requires it. But if you have a mortgage, your lender will. Once the mortgage is paid off, going without coverage means paying out of pocket for any damage, which is why most homeowners keep it indefinitely.

-

Can I bundle home and car insurance through Jerry?

Yes, and not just with the same insurer. Jerry lets you pair the best home policy from one carrier with the best car policy from another, or bundle them both under one insurer for a multi-policy discount, whichever costs less. Most Jerry customers who bundle save up to 40% compared to their previous policies.

-

Does home insurance cover roof damage?

It depends on the cause. Damage from storms, hail, falling trees or fire is typically covered. Damage from age, wear or neglect isn’t. If your roof is over 20 years old, some insurers will only pay actual cash value (what your old roof is worth today) instead of the cost of a new roof. It’s worth checking your policy’s roof clause before storm season.

-

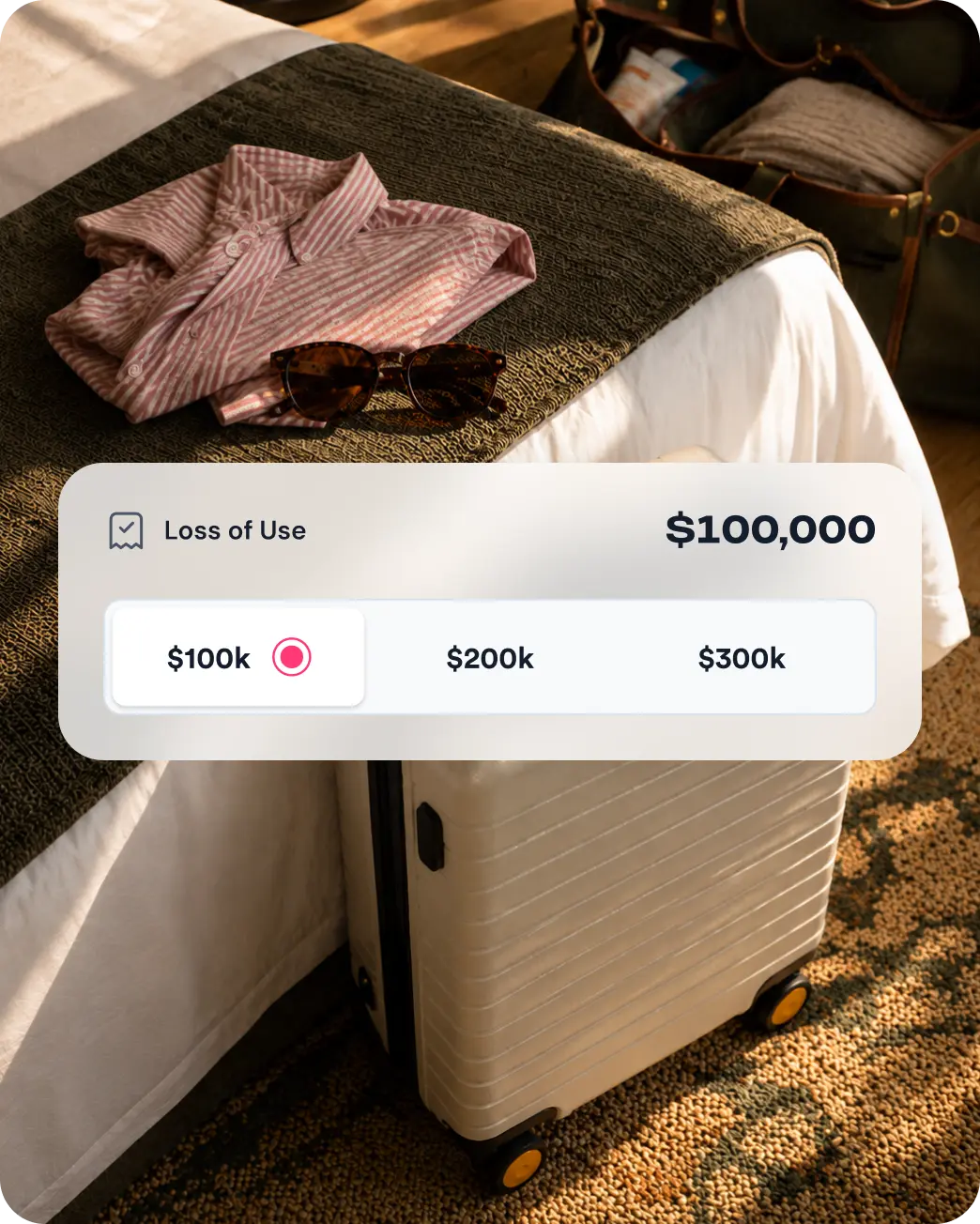

Does home insurance cover water damage?

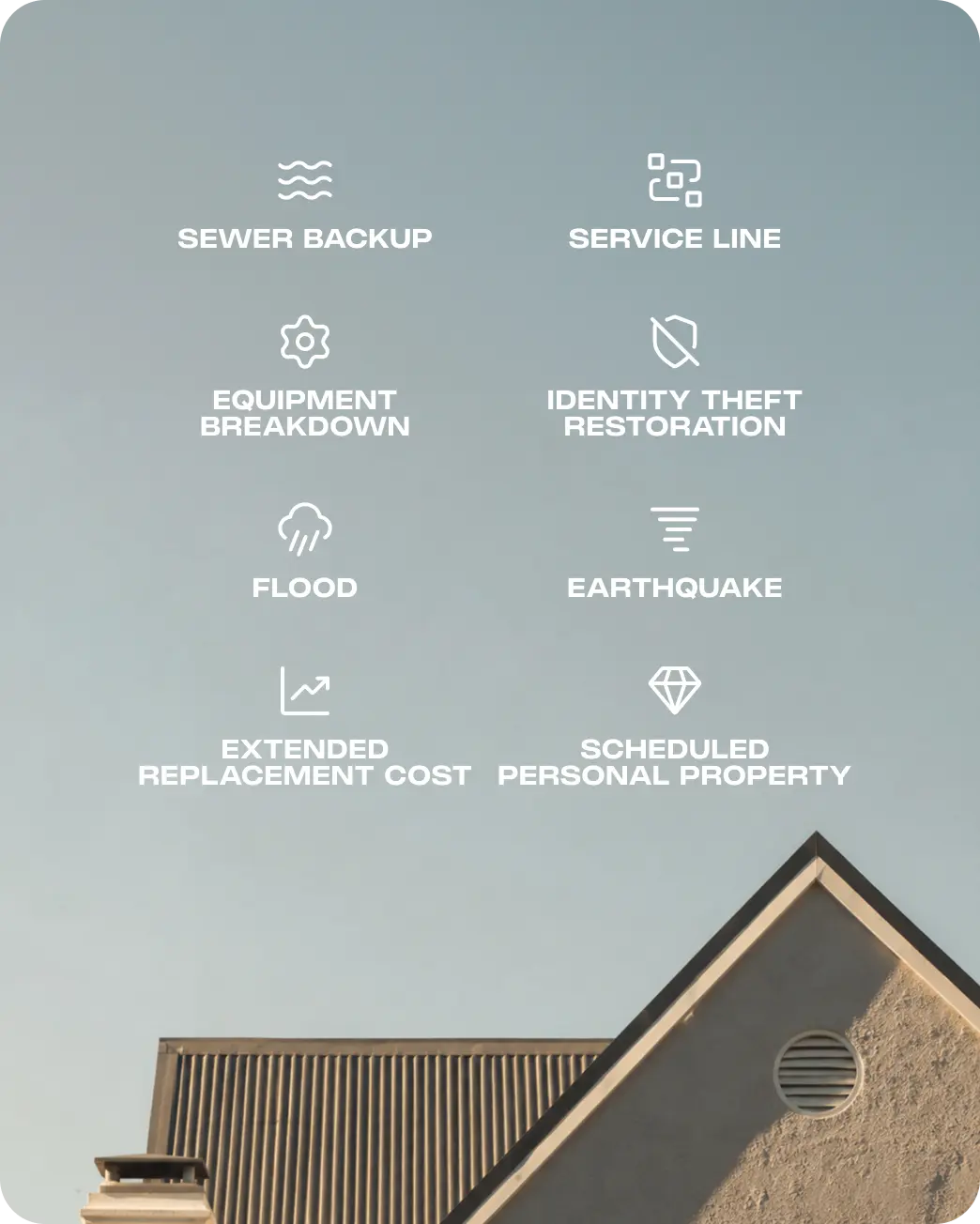

Sudden, accidental water damage, like a burst pipe or an overflowing tub, is typically covered. Floods from rising water, sewer or sump-pump backups, and slow leaks usually aren’t. Floods need a separate policy through the National Flood Insurance Program or a private carrier. Water/sewer backup is a low-cost endorsement most homeowners should add to their base policy.

-

What is replacement cost vs. actual cash value?

Replacement cost pays what it would take to replace damaged property with new equivalents at today’s prices. Actual cash value pays less, since it subtracts depreciation for age and wear. Replacement cost coverage costs more in premium but is what most homeowners actually want, especially for the home itself and major belongings.