COMPARE CAR

INSURANCE FROM

100+ INSURERS

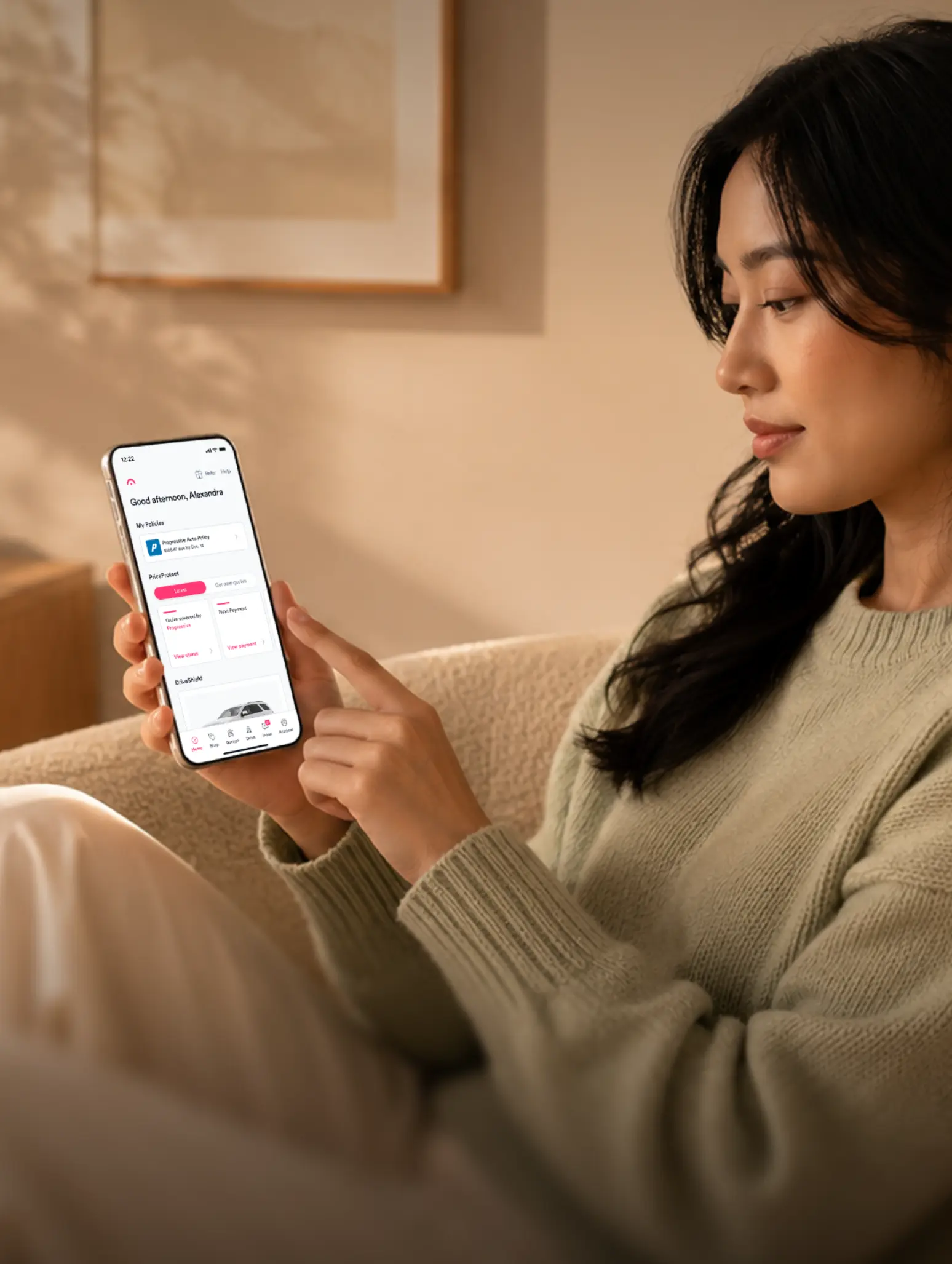

JERRY MAKES CAR INSURANCE SHOPPING EASY

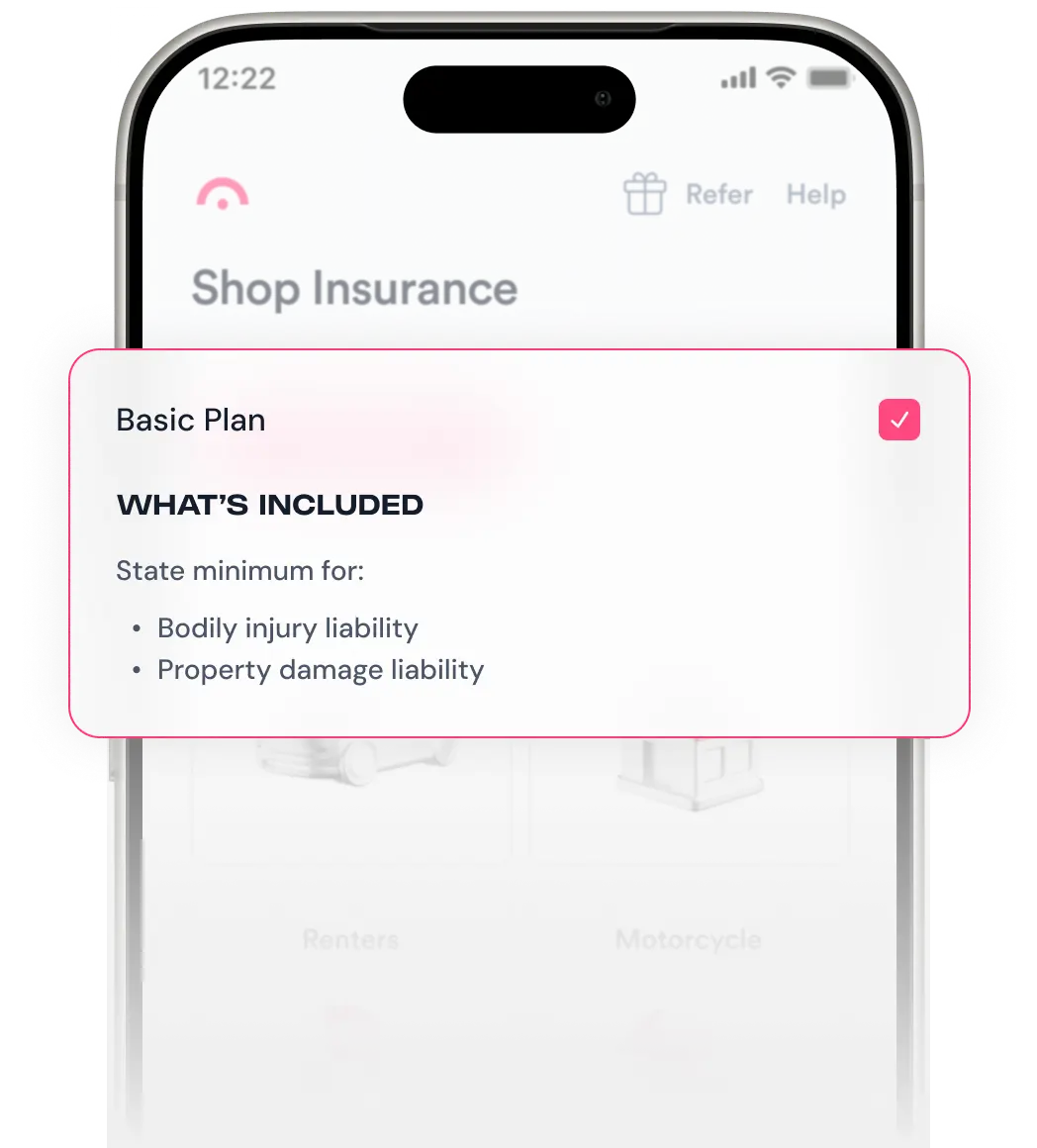

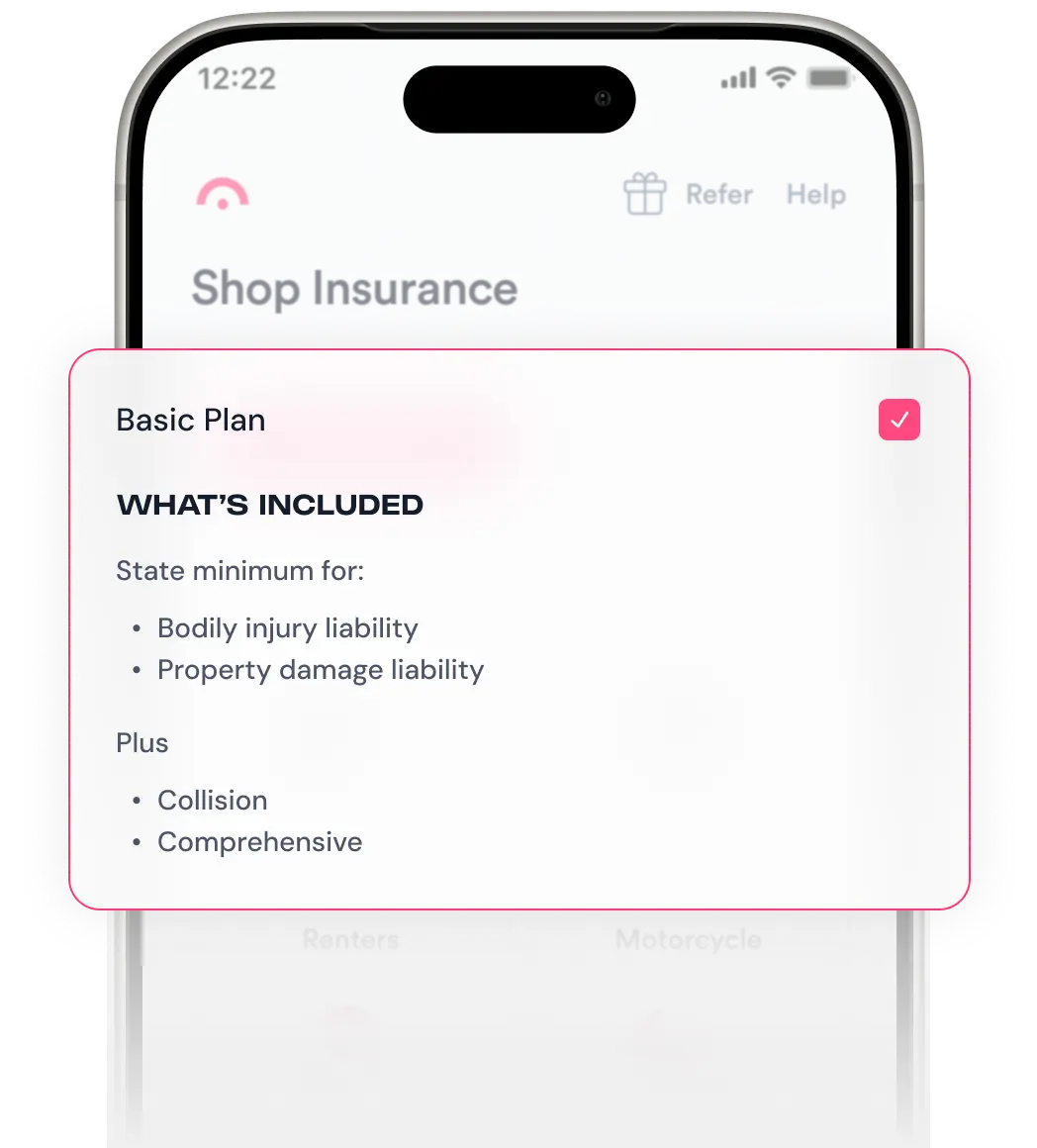

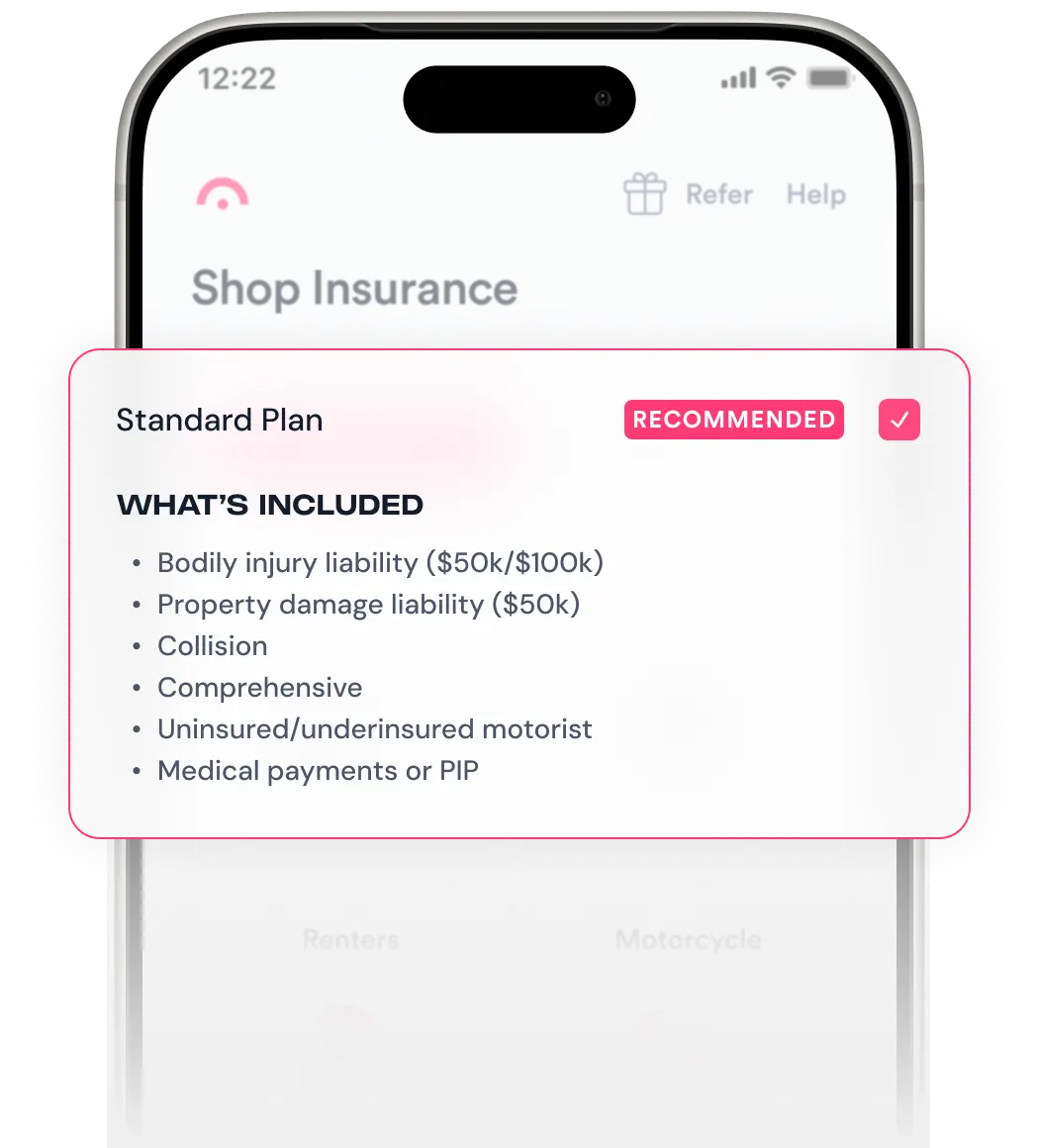

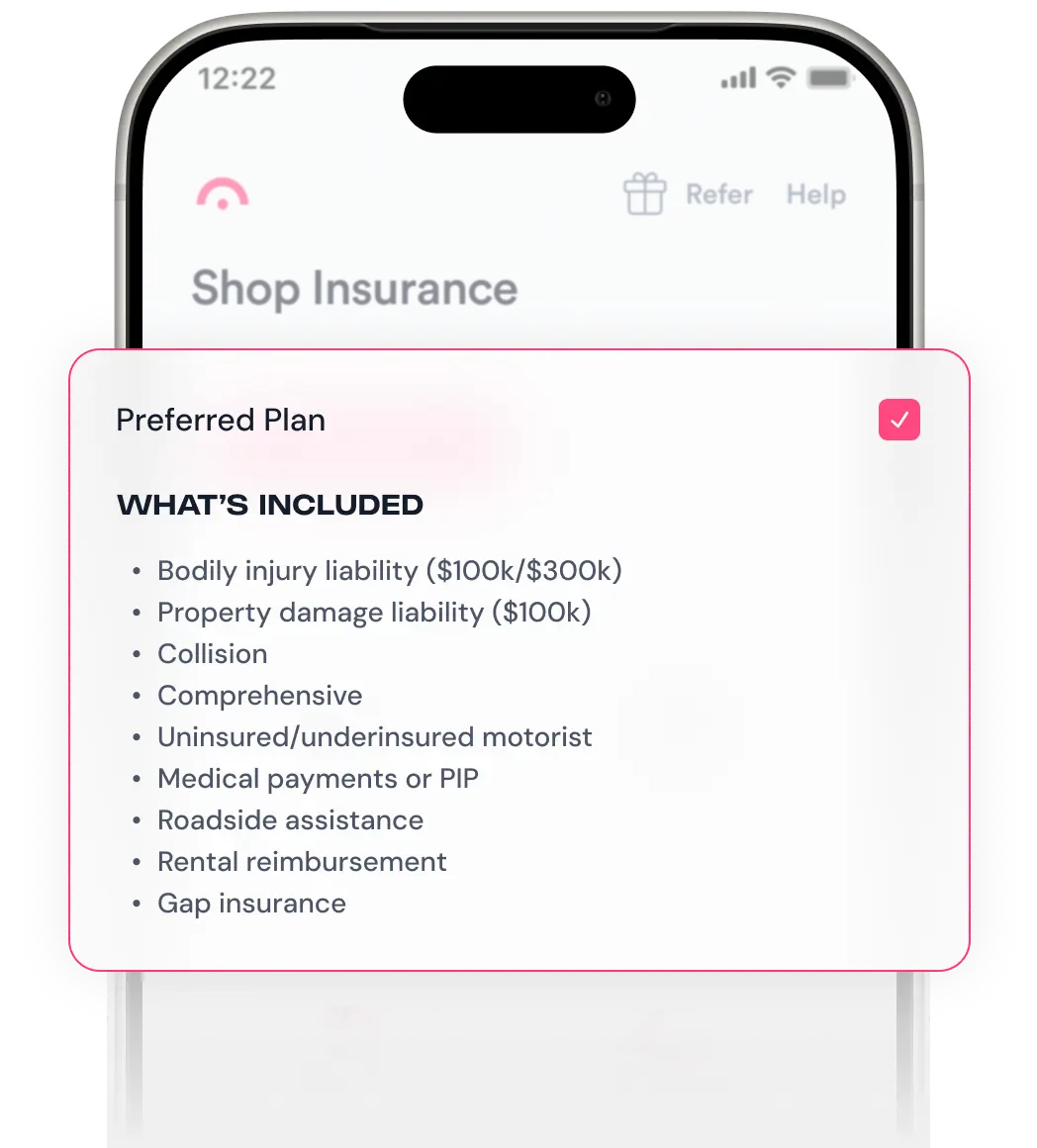

WE FIND THE RIGHT COVERAGE FOR YOU

MIX AND MATCH INSURERS TO SAVE EVEN MORE

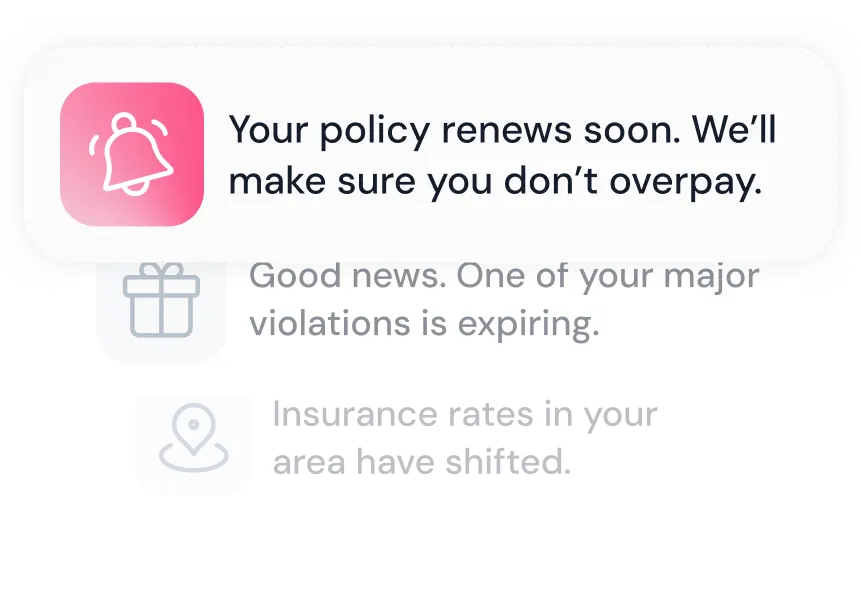

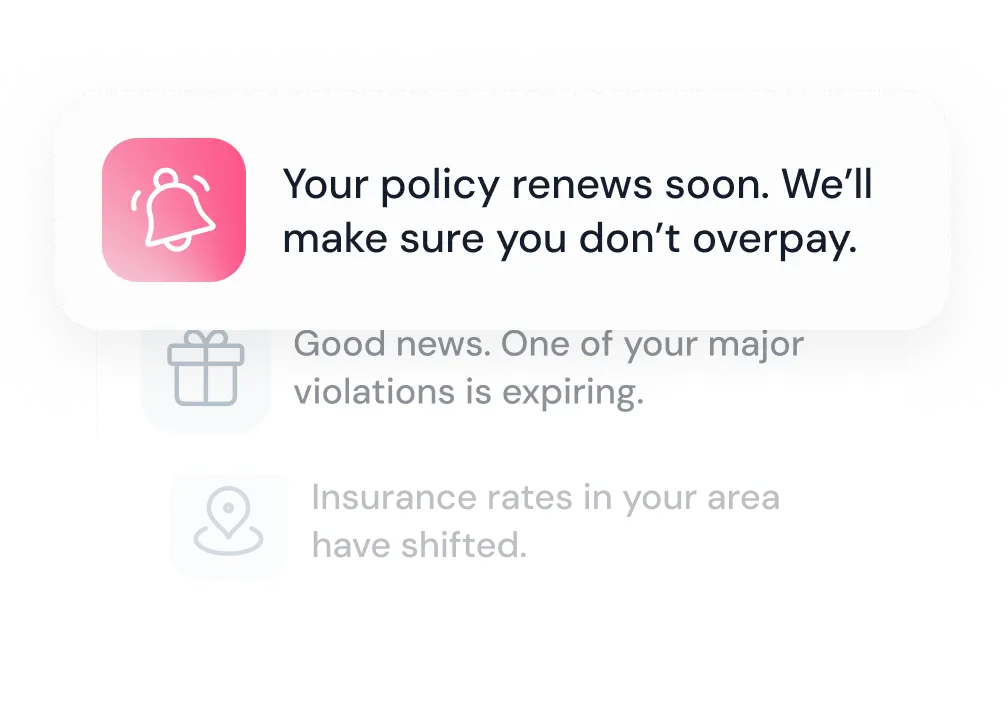

YOUR DISCOUNTS ARE AUTOMATICALLY STACKED

SHOP SMARTER WITH EXPERT RESOURCES

OVER 5 MILLION CUSTOMERS TRUST JERRY

"Jerry reduced an hours-long task to 15 minutes, and I was impressed. It’s not only fast, but it’s also comprehensive."

"My son just got his license and I was stressing about insurance costs. Downloaded Jerry and, no lie, best thing that's ever happened to me.”

"As a college student I really want cheap car insurance, and when I downloaded Jerry I saved over $100 a month.“

COMMON QUESTIONS

-

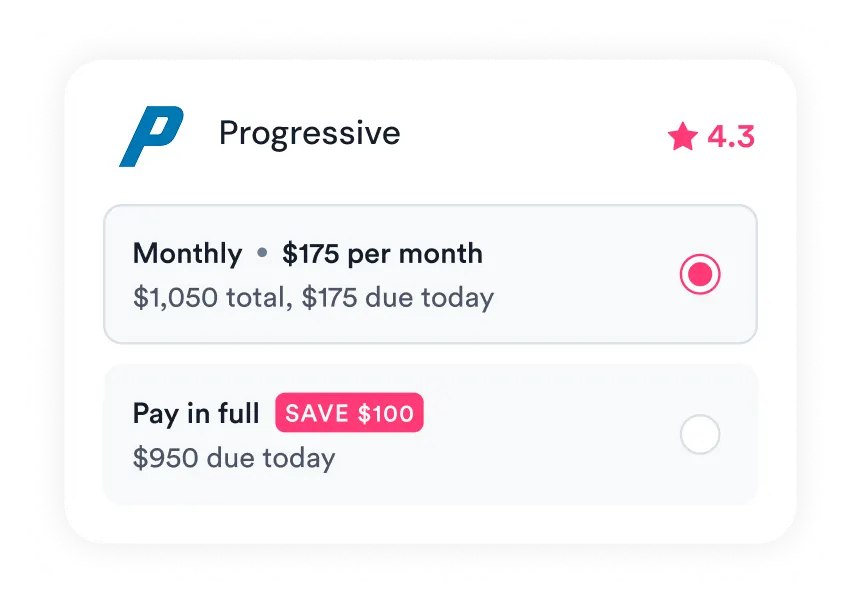

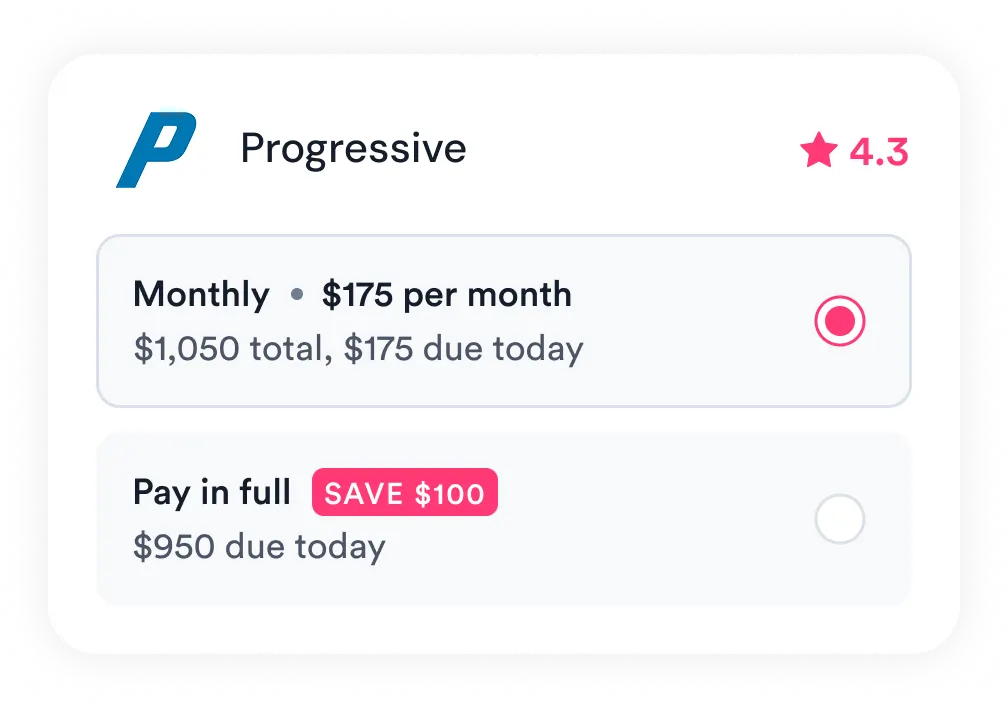

How does Jerry compare car insurance quotes?

Jerry pulls real-time quotes from 100+ insurers, all in one app. Answer a few questions about you and your car, then see side-by-side prices and coverage. You can adjust limits and deductibles to watch the price change, and when you find a policy you like, buy and switch right in the app. Jerry can even cancel your old policy for you so there’s no lapse in coverage.

-

Is Jerry actually free to use?

Yes. Comparing quotes and switching in the app is free. Jerry is a licensed insurance broker and earns a commission from the insurer when you buy a policy, the same way any broker does. In some states, we may also charge a broker fee. Jerry never sells or shares your data for marketing purposes, so there are no spam calls after your quote.

-

How much does car insurance cost per month?

Jerry customers typically pay between $125 and $241 a month, but your rate depends on your state, vehicle, driving record, age, credit-based insurance score (in most states), and how much coverage you buy. Comparing quotes now is the fastest way to know what you’d actually pay.

-

Will shopping with Jerry affect my credit score?

No. Comparing and buying through Jerry won’t affect your credit. Insurers may run a soft credit pull to generate quotes, but soft pulls are invisible to lenders and leave your score untouched.

-

Can I get covered the same day?

Yes. You can compare, pick a policy and get covered entirely in the app, usually in one sitting and in 30 minutes or less.